Renewables melting pot: diverging support costs for Pot 1 technologies

Large differences in the cost of supporting onshore wind and solar may emerge in the GB Contracts for Difference.

The GB renewable industry eagerly awaits the Contracts for Difference (CFD) auction, expected towards the end of 2021. Onshore wind and solar, as well as other established technologies [1], will be able to participate in the auction for the first time since 2015. The Government aims to deploy 12 GW of renewable capacity[2], a share of which will be available for these technologies. While maintaining value for money to the consumer, the Government hopes that re-introducing onshore wind and solar into the CFD will create the sustained growth in these sectors required for a net zero pathway. But does a competitive auction based on strike prices incentivise projects that will deliver at the lowest cost to the consumer?

At AFRY, we project that, despite being awarded the same strike price in a given auction, there is a growing gap between the cost of supporting different established technologies through the CFD.

Strike prices are only half of the story

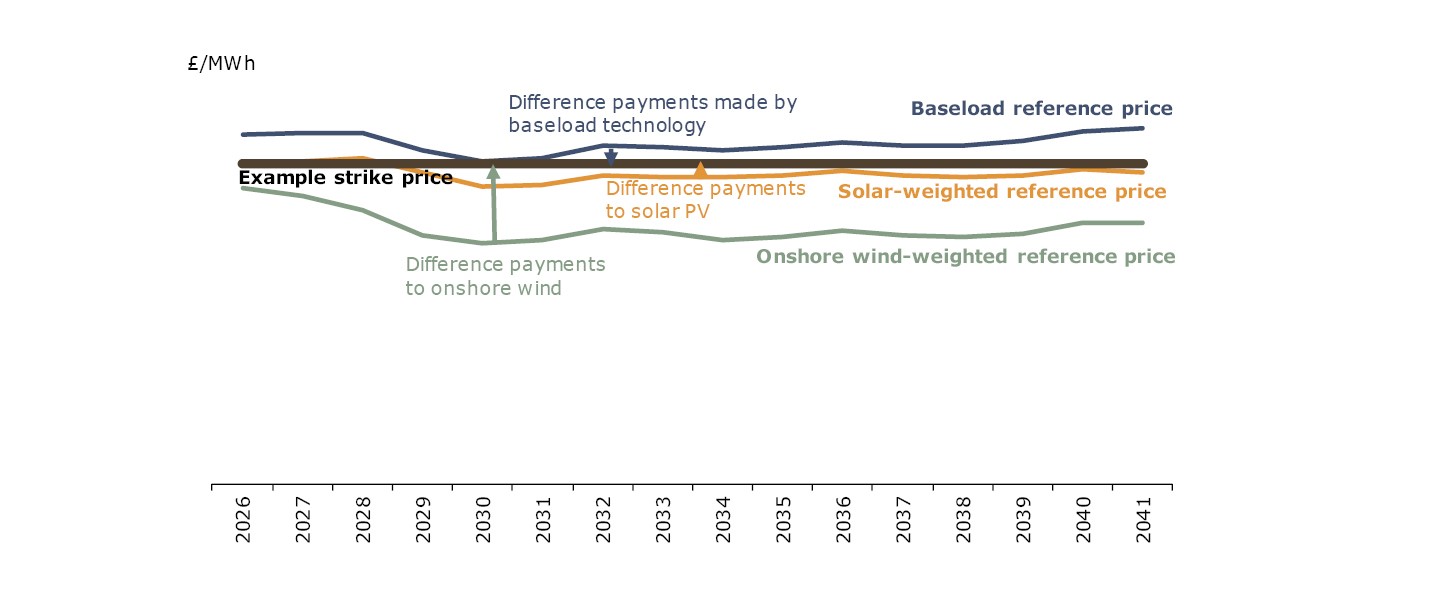

In the GB CFD, established technologies, such as onshore wind, solar PV and some waste technologies are in the same ‘pot’. They compete against each other for a contract and successful projects receive the same strike price[3], at the clearing price of the auction. This is flat[4] (in real terms) for the duration of the contract. Projects that bid below the clearing strike price will be awarded a contract[5]. Successful projects are paid the difference between the strike price and reference price, a measure of the market price of electricity. If the reference price goes above the strike price, generators pay back the difference.

As the auction is based on strike prices, it does not consider the cost of supporting each project, which is the difference between the strike price and the reference price. In the future, AFRY projects that generation-weighted realised reference prices will vary significantly by technology, leading to a large difference in support costs.

The cost of cannibalisation

The reference price for wind and solar is based on a day-ahead hourly reference price. Generation patterns therefore play a significant role. If a project generates greater volumes during low-priced hours, the generation-weighted reference price will be lower and the support costs higher, and vice versa.

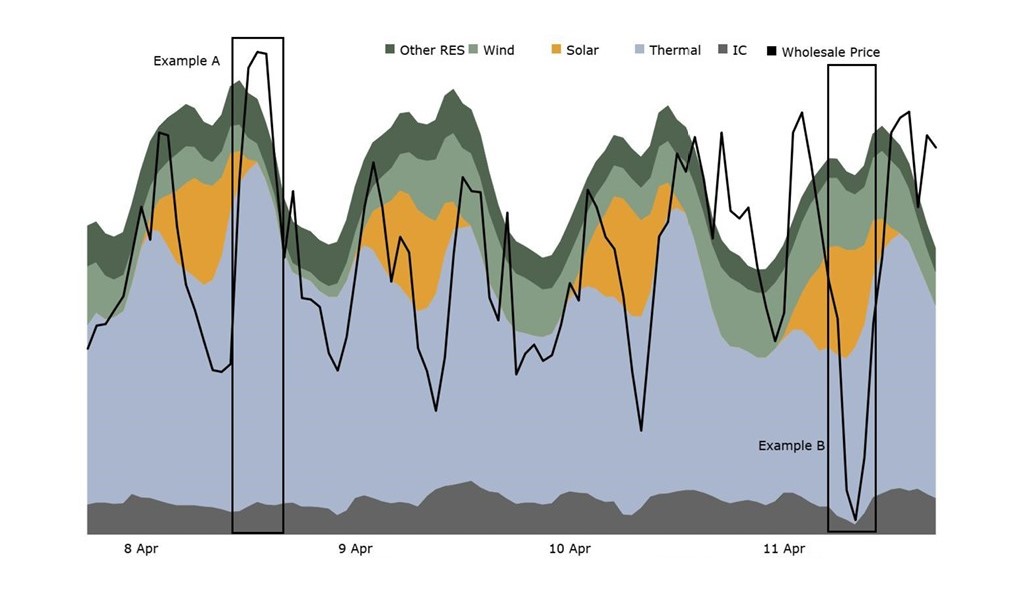

Generally, we expect the reference price that intermittent renewables capture to be lower than the baseload price due to ‘price cannibalisation’. Prices tend to be lower when renewables generate the most as they displace higher marginal cost technologies (example B in image). Conversely, when renewable output is low, this tends to force higher cost generation sources to operate, pushing up prices (Example A in image). The closer a project’s generation pattern is with the aggregate renewable generation across the country, the greater price cannibalisation is expected.

Although there are high expectations for the capacity of onshore wind and solar to be procured through future CFD auctions, it is offshore wind that has taken centre stage in recent policy announcements, with a target of 40GW offshore wind by 2030. This will almost quadruple the capacity of offshore wind installed today.

Unsurprisingly, onshore wind generation patterns tend to correlate closely with offshore wind. This increase in offshore wind generation could have a substantial impact on cannibalisation of prices for onshore wind over the next decade. Couple this with higher demand during the day, when solar generates, and this leads to significantly higher captured reference prices for solar than onshore wind and, conversely lower support costs.

Technologies such as Energy from Waste with CHP, Landfill gas and Sewage gas will also compete against onshore wind and solar in Pot 1. These technologies receive a reference price based on season-ahead forward prices. As such, without any price cannibalisation, AFRY projects higher reference prices than wind or solar for these technologies, and hence, lower support costs.

There are many elements that will contribute to the exact support costs, and the future capacity mix is a key factor for determining the levels of cannibalisation. Ultimately different renewable technologies tend to be complementary, and a range of technologies will likely lead to lower support costs. The trend shown here is based on AFRY’s current capacity outlook but would change if the balance between solar and wind changed significantly.

Do we expect change?

Beyond the 2021 auction, CFD auctions are expected every other year. The Government have recently published a Call for Evidence ‘Enabling a high renewable, net zero electricity system’. This aims to understand how to incentivise generators to minimise overall system costs of large amounts of renewables. One area explored is price cannibalisation and this may lead to reform of the CFD. However, the CFD has been deemed a very successful instrument in deployment of offshore wind, which could mean there is some reluctance to change.

Notes

[1] Energy from Waste with CHP, Hydro (>5MW and <50MW), Landfill gas and Sewage gas, Onshore wind (>5MW) and Solar PV (>5MW).

[2] Government’s aim for all renewables procured from allocation round 4, including offshore wind, subject to sufficient projects coming through the planning pipeline to maintain competitiveness.

[3] Administrative strike prices place a cap on the strike price which can be received by each technology, which could lead to differences in strike prices. Historically, strike prices could be different across different delivery years (although this may change for allocation round 4).

[4] Strike prices are indexed to CPI and adjusted for changes to BSUoS and transmission losses.

[5] Subject to maxima and minima which may be applied to certain technologies.

If you have any questions, please get in touch with Katie Potter and Susan Stead.